Benefit from a more volatile market

The Levendi Thornbridge Defined Return Fund was one of a small number of Funds to offer a positive return through 2018, demonstrating the all-weather nature of the strategy. Looking forward the Fund gives investors a chance to benefit from increased volatility and lower market levels. The Fund offers the possibility of positive returns which do not rely on rising markets and offers significant protection if markets continue to slide.

THREE REASONS TO INVEST IN THE FUND

- Capture higher levels of implied volatility and lower market levels.

- Transparent strategy; No equity market growth required for positive returns and protection against losses at maturity of each investment

- Active risk management

BENEFIT FROM HIGHER VOLATILITY AND LOWER MARKET LEVELS

Falling markets and the increase in realised volatility has been one of the defining features of the fourth quarter of 2019. Realised volatility has increased across all main equity market indices, driven by multiple factors that we think will continue to be relevant through 2019. The list of contributory factors includes Chinese economic slowdown, the level of personal and government debt, worries about liquidity, trade wars, quantitative tightening, US rate rises, slowdown in US earnings growth and of course Brexit. Unless there is a seismic shift in global macro policy there is no reason to suppose that volatility will not remain elevated for a while yet. Many forecasters have higher volatility as one of the main themes for 2019 and beyond.

Arguably, current market conditions and the outlook for 2019 makes this one of the most favourable entry points to the Fund since it was launched. Increased implied volatility and lower markets both improve the risk/return profile of the Fund. Higher realised volatility has driven up the level of implied volatility and therefore improves the returns of new assets the Fund can buy. In addition to this, the Fund can now buy new investments which will also benefit from lower strike levels. The impact of both factors on the valuation of existing assets held by the Fund means that new investors in the Fund immediately benefit from current market conditions.

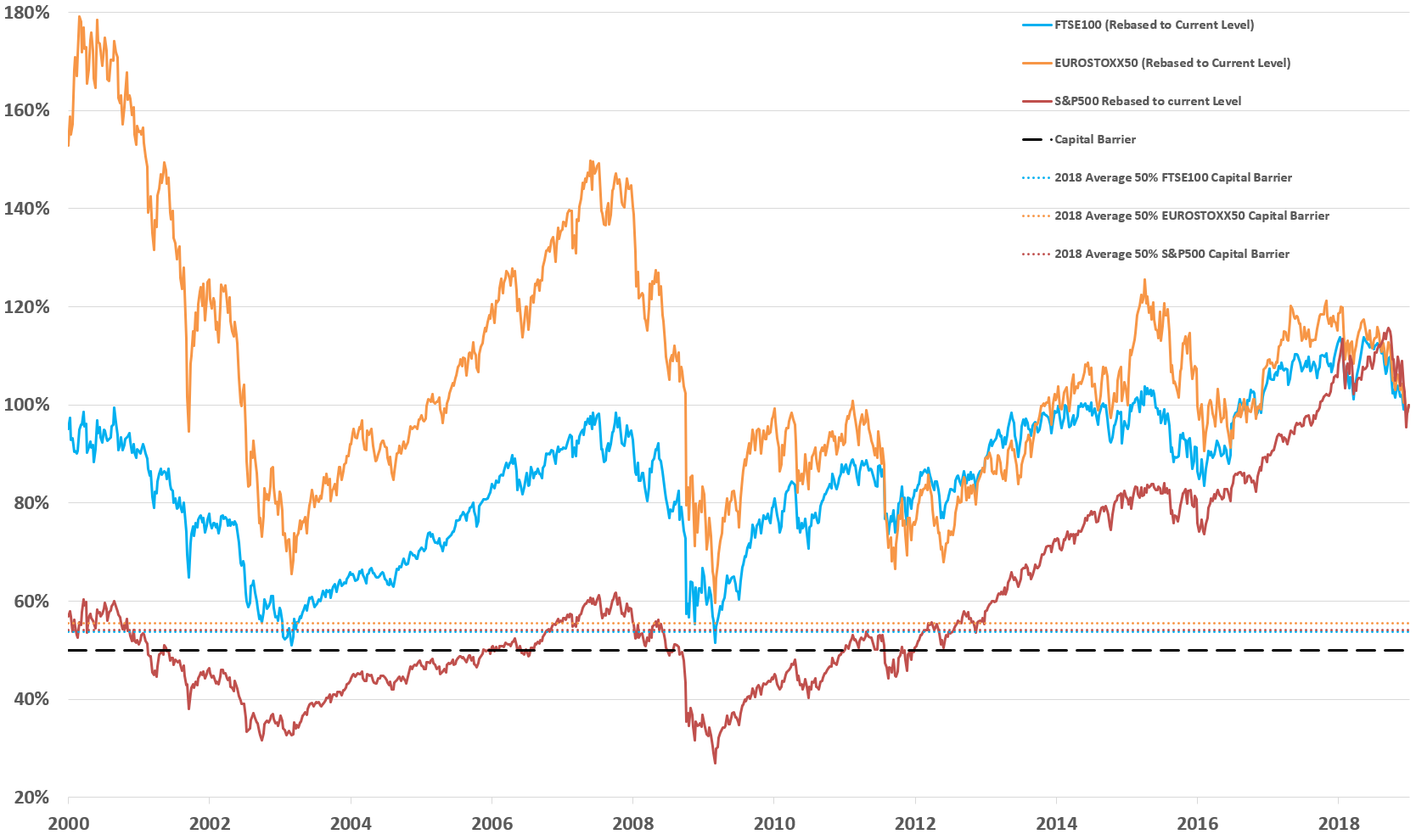

FTSE 100, S&P 500, EUROSTOXX 50 INDEX LEVES REBASED SO LAST VALUE IS 100%

Source; Levendi Investment Management, Bloomberg

The chart above displays the levels of the FTSE100, Eurostoxx50 and S&P500 all rebased so that the January 2019 value is 100%. This chart makes it easy to see how far markets would have to drop to hit the Capital barriers. The chart shows the 50% Barrier based of the latest value as well as 50% Barriers for the average levels through 2018 of each Index.

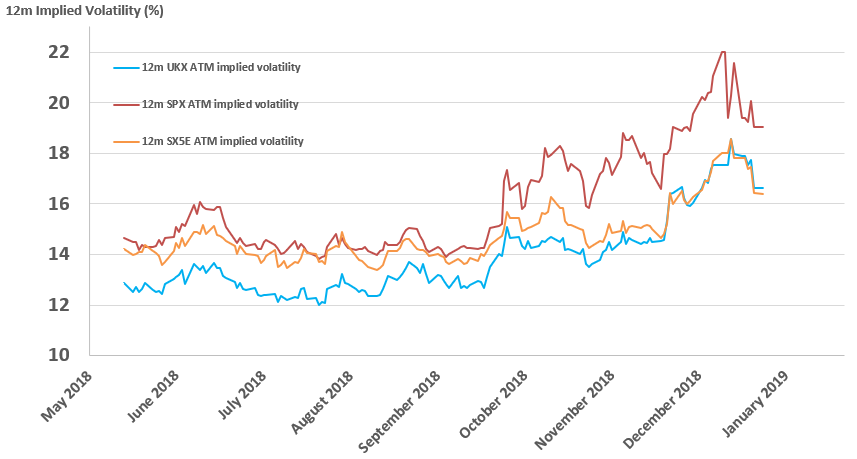

12M AT THE MONEY IMPLIED VOLATILITY

Source; Levendi Investment Management, Bloomberg

The levels of implied volatilities of the FTSE100, Eurostoxx 50 and S&P500 options have increased significantly over the last 6 months.

TRANSPARENT STRATEGY; NO GROWTH REQUIRED FOR POSITIVE RETURNS

A key benefit of the Levendi Fund when compared with other absolute return Funds, is the transparency it offers to investors. The assets held have a defined return. The payoff and the condition required to generate the return are known in advance. The circumstances where there may be no payoff, or a loss are known with certainty. Typically, everything depends on the level of main equity market indices.

A significant majority of the assets the fund holds have been developed specifically for the fund. They are developed to maximise the chance of generating a positive return and minimising the chance and scale of losses.

Typically, in order to receive the maximum return possible from an asset we hold, all that we require is that equity markets do not fall by more than 40% over an eight-year term. There are early maturity conditions that can result in the asset paying out at earlier anniversaries. Falls of this magnitude over this timetable are very rare indeed. The only instance they have occurred is from the back end of the Dot-Com peak in early 2001 to the depths of the Financial Crisis in 2009.

For the assets we hold to mature at less than 100% the underlying equity markets would typically need to fall by more than 50% over an eight-year period. This would take both the FTSE 100 and Eurostoxx 50 below the lows of both the Financial Crisis and the Dot-Com crash. Although not impossible, this is a very remote risk in our opinion and one that we are comfortable with.

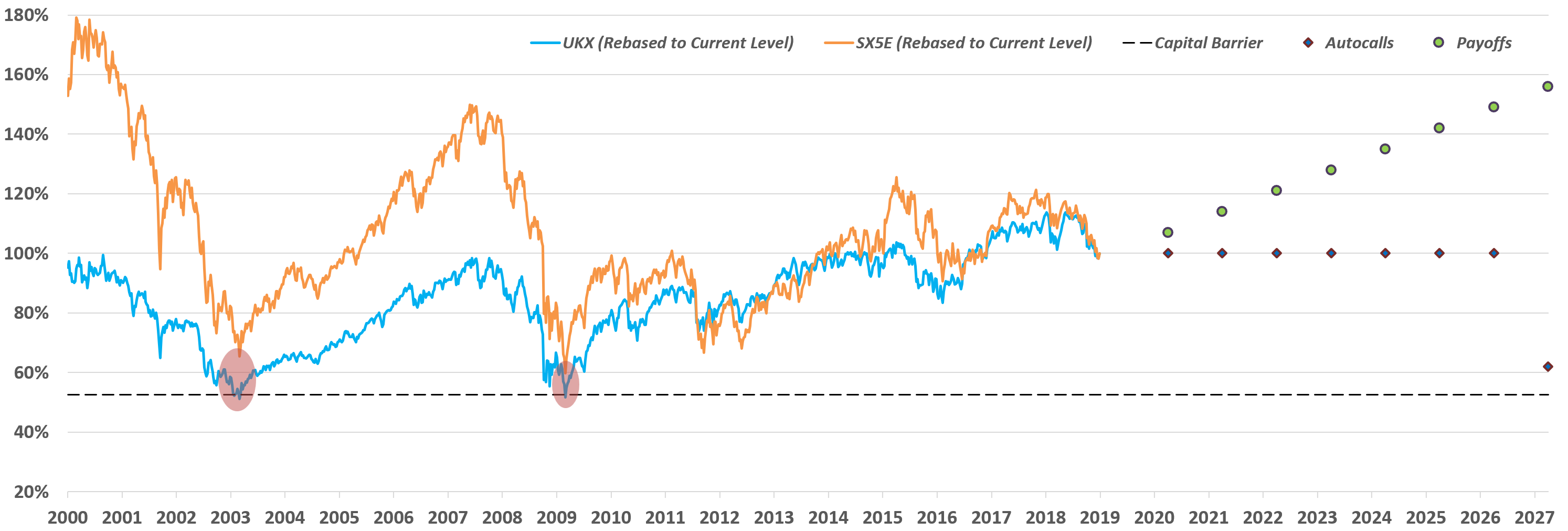

AUTOCALL / PUT STRIKE LEVELS AND PAYOFF FOR TYPICAL LEVENDI INVESTMENT

Source; Levendi Investment Management, Bloomberg

The chart illustrates the typical terms of products held by the Fund. The FTSE100 and Eurostoxx50 are rebased so that the last value is 100%. In this case the product offers a return of 7% for each year up to the (early) maturity date. The product can mature early each year if both indices are above 100% of the initial level. At the maturity date, the condition for payment of the 56% return due at that date is that both markets are above 60% of the initial level. The put strike is 50%. The maturity value will only be less than 100% if one of the indices falls by more than half over eight years.

ACTIVE RISK MANAGEMENT

Wealth preservation is at the heart of our investment strategy. We are acutely aware of the risks that we face. The risks are clear, defined, measurable and can be hedged if we need to. We have strategies to mitigate the risks while preserving the opportunities to generate an attractive return. These include the choice of underlying market exposure, the design of the assets we hold and our risk management overlay.

We don’t need to select the markets that perform the best, but simply avoid markets we think have significant downside risk. This has meant that to-date we have focused on the FTSE 100 and Eurostoxx 50. In our opinion they are the two markets that in our opinion offered the best combination of product terms and downside risk. We have avoided any US exposure so far, because of elevated valuations. We have not included any Emerging Market exposure because of risks of Chinese slowdown, impact of changes in the value of the US Dollar and the effects of changing US monetary policy.

The increased level of realised volatility through the 4th quarter meant that we used our risk management overlay. This process allows us to remain fully invested and to dampen down the effect of higher market volatility on the NAV of the Fund and offset the impact of rising volatility on the mark-to-market of existing assets. The overlay has added over 0.4% to the NAV of the Fund and meant that realised volatility of the Fund has remained below 6%.

CONCLUSIONS

The current hiatus offers investors an attractive opportunity to invest in the Levendi Thornbridge Defined Return Fund. The performance of the Fund through 2018 has shown that the Fund can generate positive returns through one of the worst years since the Financial Crisis. The change in market conditions at the end of 2018, specifically the fall in the level of markets and the increase in volatility means that this is a very attractive time to invest in the Fund. The Fund can be used as part of an investor’s equity allocation or instead of absolute return funds.

DISCLAIMER

The contents of this document are communicated by, and the property of, Levendi Investment Management Ltd. Levendi Investment Management Limited Ltd is an appointed representative of Thornbridge Investment Management LLP which is authorised and regulated by the Financial Conduct Authority (“FCA”). The information and opinions contained in this document are subject to updating and verification and may be subject to amendment. No representation, warranty, or undertaking, express or limited, is given as to the accuracy or completeness of the information or opinions contained in this document by Levendi Investment Management Ltd or its directors. No liability is accepted by such persons for the accuracy or completeness of any information or opinions. As such, no reliance may be placed for any purpose on the information and opinions contained in this document. The information contained in this document is strictly confidential. The value of investments and any income generated may go down as well as up and is not guaranteed. Past performance is not necessarily a guide to future performance.