Comparison of product Fair Values

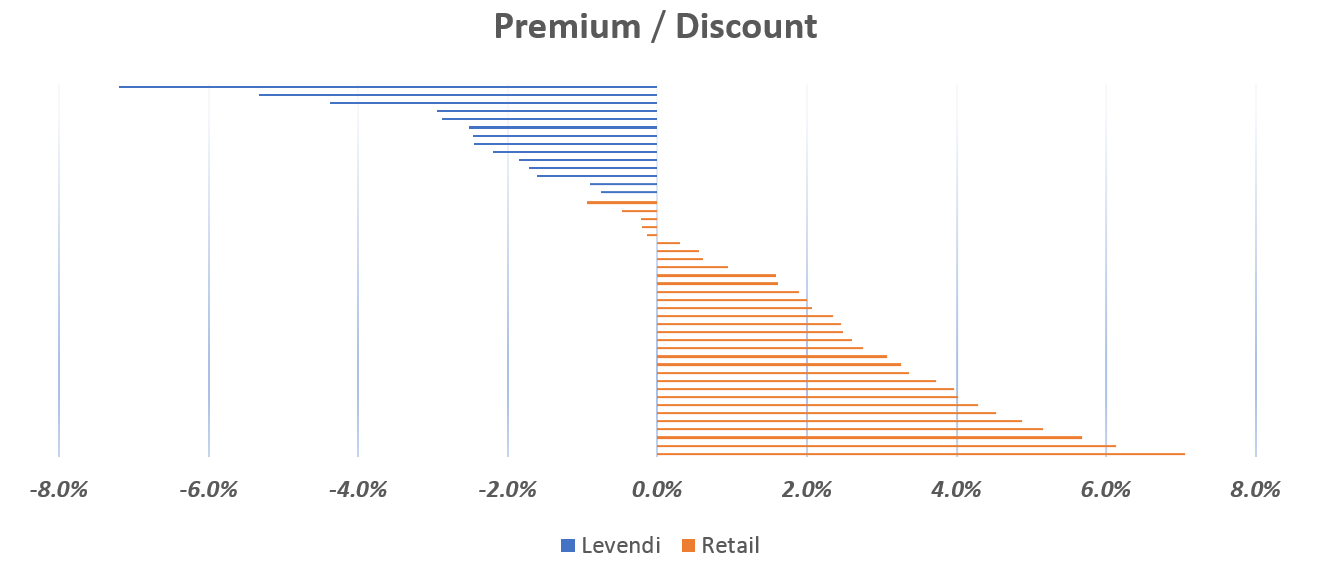

Comparing the premium or discount to fair value of retail structured products and the products held by Levendi Thornbridge Defined Return Fund (8th November 2018)

SUMMARY

Retail investors looking to invest in Structured Products now have a choice between owning individual Structured Products and investing in a fund of structured products like the Levendi Thornbridge Defined Return Fund. In this paper, we compare the relative costs of structured products to a “Fair Value”. Our analysis shows that on average Retail Plans are offered at a premium to Fair Value and that products held in the Levendi Fund trade are typically purchased at a discount to the same calibrated Fair Value. It follows that investors buying the Levendi fund are potentially picking up a sizable cost benefit, and in some cases, as much as 5% of the overall cost.

THE TWO PRODUCT SETS

To try and ensure that we are comparing apples with apples we have selected the two product sets so that they are equivalent. Aside from setting the basis for inclusion in this study, we have not refined or filtered the products that are included.

RETAIL PRODUCTS

Our universe of retail products is a representative set of non-deposit products available to UK retail investors.

LEVENDI PRODUCTS

The Levendi products are the Notes currently held in the Fund. The investments of the Fund are split between Notes and OTC contracts. We have selected the Notes because these are the most directly comparable assets with retail plans. The notes held in the Fund are closely comparable to the assets held in a retail structured product plan. They are securities issued by a bank.

FAIR VALUE

The purpose of this study is to try and identify a persistence and scale of a cost premia or discount of each product relative to its the “Fair Value”. The Fair Value of a product is in reality a nebulous concept. The Levendi models calculate the value of a product in much the same way to that of the issuing banks. Levendi uses market data for implied volatilities, forwards, implied correlations, interest rates and the other inputs that are required for independent product pricings. Additionally, issuers of structured products will adjust and tweak their pricing models to take into account additional costs, such as, but not limited to, implied costs of hedging, regulatory capital, internal funding and issuance costs. Finally, they will also include a margin. Levendi tries to replicate such adjustments and in doing so, have calibrated internal model so that we can estimate the product terms that issuers will offer for a new product that is being offered to professional investors.

The Fair Value calculation can provide a credible yardstick by which to measure the estimated value of a product. In this report, we describe products that are valued below the fair value estimates and trading at a discount and describe products that are valued above the fair value measure and trading at a premium.

RESULTS

The results of our study are shown in the chart above.

| Retail Products | Levendi Products | |

| Total products | 32 | 14 |

| Average Premium / Discount | 2.5% premium | 2.8% discount |

| Highest Premium | 7.1% | -0.8% |

| Largest Discount | -0.9% | -7.2% |

CONCLUSIONS

Identifying the persistence and scale of products offered at a premium or discount to fair value is an important consideration when investing in structured products, as in any investment. Products trading at a lower premia or larger discounts to the estimate fair values are, in general, likely to offer better potential returns.

The issuer fees when purchasing retail plans are typically on average circa. 2.5%, which appears fair for product that may last up to 6 years and in some cases 10 years. Such costs include the costs of administration, valuation and custody over the life-time of the product.

This analysis shows that investors purchasing the Levendi Fund are, on average, accessing products at a more competitive level than when purchasing via retail plans. In this study, the cheapest retail product is indicatively offered for secondary trading at a discount of 0.9% to the fair value. Whereas, the most expensive product held in the Levendi Fund is indicatively offered at a discount of 0.8% to the fair value.

There are several reasons why the Fund can buy the same products at a more competitive rate. The main factor is that the issuer deals with Levendi as a professional investor. There are none of the fees, charges or margins associated with issuing retail plan. Issuers will typically incur more costs and regulatory reporting requirements when issuing to retail investors and so must charge for the additional workload.

The Levendi Fund is available to retail investors. There are two share-classes, an accumulation and a distribution share-classes which pays 5% per year. If you would like to know more about the Fund then please contact David Stuff.

Email; david.stuff@levendi-im.com

Telephone; 0203 150 2847

DISCLAIMER

The contents of this document are communicated by, and the property of, Levendi Investment Management Ltd. Levendi Investment Management Limited Ltd is an appointed representative of Thornbridge Investment Management LLP which is authorised and regulated by the Financial Conduct Authority (“FCA”). The information and opinions contained in this document are subject to updating and verification and may be subject to amendment. No representation, warranty, or undertaking, express or limited, is given as to the accuracy or completeness of the information or opinions contained in this document by Levendi Investment Management Ltd or its directors. No liability is accepted by such persons for the accuracy or completeness of any information or opinions. As such, no reliance may be placed for any purpose on the information and opinions contained in this document. The information contained in this document is strictly confidential. The value of investments and any income generated may go down as well as up and is not guaranteed. Past performance is not necessarily a guide to future performance.